If you’re looking for creative ways to fund a client’s LTC premiums, we’ve included two of them below. To discuss in more detail, contact Scott Simpson,

- Email: scott.simpson@lifeinsservices.com

- Office: 704.927.0101

- Cell: 704.609.4570 (text or call)

Assumptions on below scenarios:

- Male 65

- LTC $5,000/month for 4 years with 3% Inflation

- IRA has $250,000 currently and is earning 4%

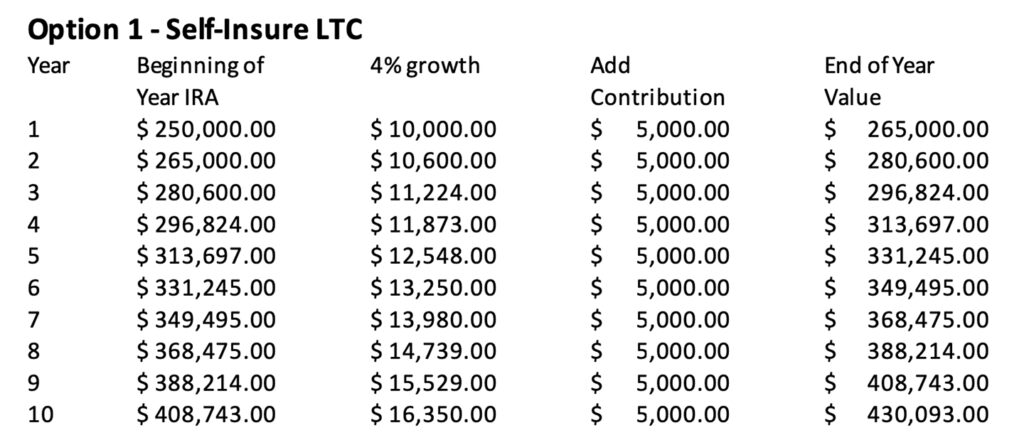

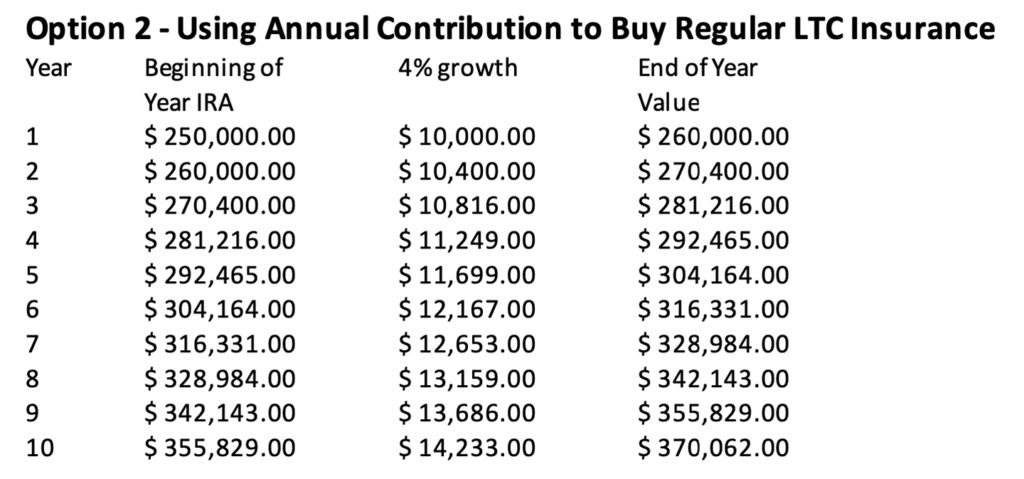

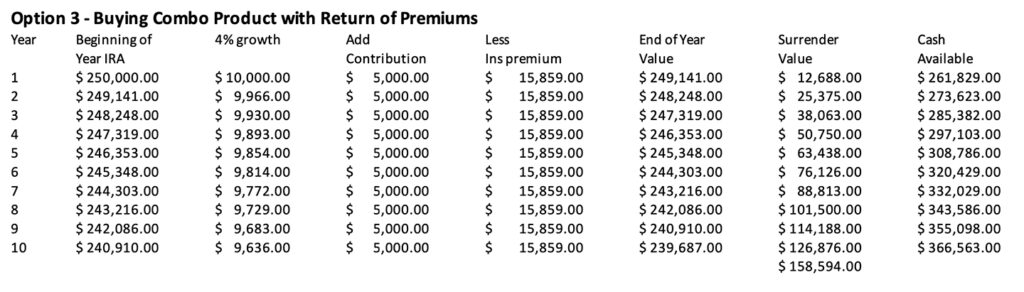

Use IRA Funds (see exhibit below for comparisons)

- Self-fund the costs when they occur

a. Pro: Highest income from IRA

b.Con: May not be adequate to cover Medicare supp premiums and LTC costs - Use the IRA to purchase normal LTC insurance

a. Pro: Minimal effect on IRA

b. Cons: Uses up IRA contribution, Premiums not guaranteed, Pay forever - Take from the IRA over ten years to buy a combo product with return of premiums

a. Pro: Everything is guaranteed, Can be surrendered after ten years for 100% of premiums paid

b. Con: Uses about 45% of IRA in ten years (but you have the surrender value if needed, which is an additional 35%)

Take Out a Home Equity Loan ($150,000 20 yrs. is about $500/month)

- Use it to buy an annuity to pay the ten premiums on a combo product again with return of premiums

a. Pro: Spreads the cost over 20 years and you have the policy surrender value after ten years to pay loan off if needed

b. Con: You have a fixed payment for 20 years - If not able to buy LTC insurance, use this to buy a deferred annuity that will grow in value and give you 2x or 3x normal income if in a nursing home

a. Pro: No underwriting and there is liquidity to pay off the home equity loan if needed

b. Con: You have a fixed payment for 20 years